Most people think pharmacies make big money off every prescription. But if you’ve ever worked behind the counter or run a small pharmacy, you know the truth: generics are the only thing keeping many of them afloat. It’s a strange system. Brand-name drugs cost hundreds or even thousands per prescription, yet pharmacies barely scratch out a profit on them. Meanwhile, a $5 generic pill-something you can buy at Walmart for less than your coffee-gives the pharmacy nearly 40% markup. That’s not a mistake. It’s the entire business model.

Why Generics Are the Real Profit Engine

In the U.S., about 90% of prescriptions filled are for generic drugs. But here’s the twist: those same generics make up only about 25% of total drug spending. The rest? Brand-name drugs, which cost far more but give pharmacies almost nothing in profit. According to the Schaeffer Center’s 2022 analysis, pharmacies earn an average gross margin of 42.7% on generics, but just 3.5% on brand-name drugs. That’s a 12x difference. Why? Because brand-name drugs are priced by manufacturers with little competition. PBMs (pharmacy benefit managers) negotiate rebates directly with those manufacturers, and pharmacies get paid a fixed reimbursement rate-often below what they paid for the drug. In some cases, pharmacies actually lose money on brand prescriptions. But generics? They’re priced differently. Since multiple manufacturers can produce the same generic, competition drives down the wholesale cost. Pharmacies buy them cheap, then charge a flat fee or percentage markup. That’s where the profit lives.The Hidden Middlemen: How PBMs Control the Game

You might think the pharmacy sets the price. They don’t. The real power lies with PBMs-companies like CVS Caremark, Express Scripts, and OptumRx. Together, they handle about 80% of all prescription claims in the U.S. They act as middlemen between insurers, pharmacies, and drugmakers. And they’ve built a system that rewards volume over transparency. One of the biggest tricks? Spread pricing. A PBM tells your insurer, “This generic costs $12.” But they only pay the pharmacy $8. The $4 difference? That’s their profit. The pharmacy doesn’t know the true cost. The patient doesn’t know. And if the pharmacy’s reimbursement rate drops later, they might get a “clawback”-a demand to pay back money they already received. One Ohio pharmacy owner told Pharmacy Times: “My net profit on generics has dropped from 8-10% five years ago to barely 2% now.” These practices are legal. But they’re not fair. Independent pharmacies have no bargaining power. Chain pharmacies survive because they own their own PBMs. Independent pharmacies? They’re stuck.Consolidation Is Killing Small Pharmacies

Between 2018 and 2023, over 3,000 independent pharmacies closed. Why? It’s not because people stopped filling prescriptions. It’s because the economics changed. The National Community Pharmacists Association found that 68% of independent owners listed declining generic reimbursement as their top threat. Even though gross margins on generics were around 25% in 2015, they’ve dropped to under 20% by 2022. Meanwhile, the top five generic drug manufacturers now control 45% of the market-up from 32% in 2015. Fewer manufacturers mean less competition. And less competition means prices can spike. In some cases, a single-source generic-where only one company makes the drug-is now more expensive than the brand-name version. SureCost’s 2024 white paper documented cases where generic prices jumped 300% overnight because no one else could produce it. Independent pharmacies can’t absorb that kind of shock. Chains can. They buy in bulk. They negotiate directly. They even own their own PBMs. That’s why CVS and Walgreens keep opening new locations while small-town pharmacies shutter.

Mail-Order vs. Retail: A Stark Divide

The gap between mail-order pharmacies and local ones is getting wider. Data from 3Axis Advisors shows that for generic drugs, mail-order pharmacies make more than four times the margin of a grocery store pharmacy. For brand drugs? Mail-order margins are over 35 times higher. And then there’s the extreme: some mail-order pharmacies make up to 1,000 times more profit on certain generics than a local pharmacy does. How? They don’t play by the same rules. They’re often owned by PBMs or insurers. They don’t have to pay rent, staff, or utilities. They process thousands of prescriptions a day with automation. The cost per prescription drops to pennies. For a single mom picking up her child’s asthma inhaler at a neighborhood pharmacy, the difference is invisible. But behind the scenes, it’s a war. Retail pharmacies are being squeezed out-not because they’re inefficient, but because the system favors scale over service.How Some Pharmacies Are Fighting Back

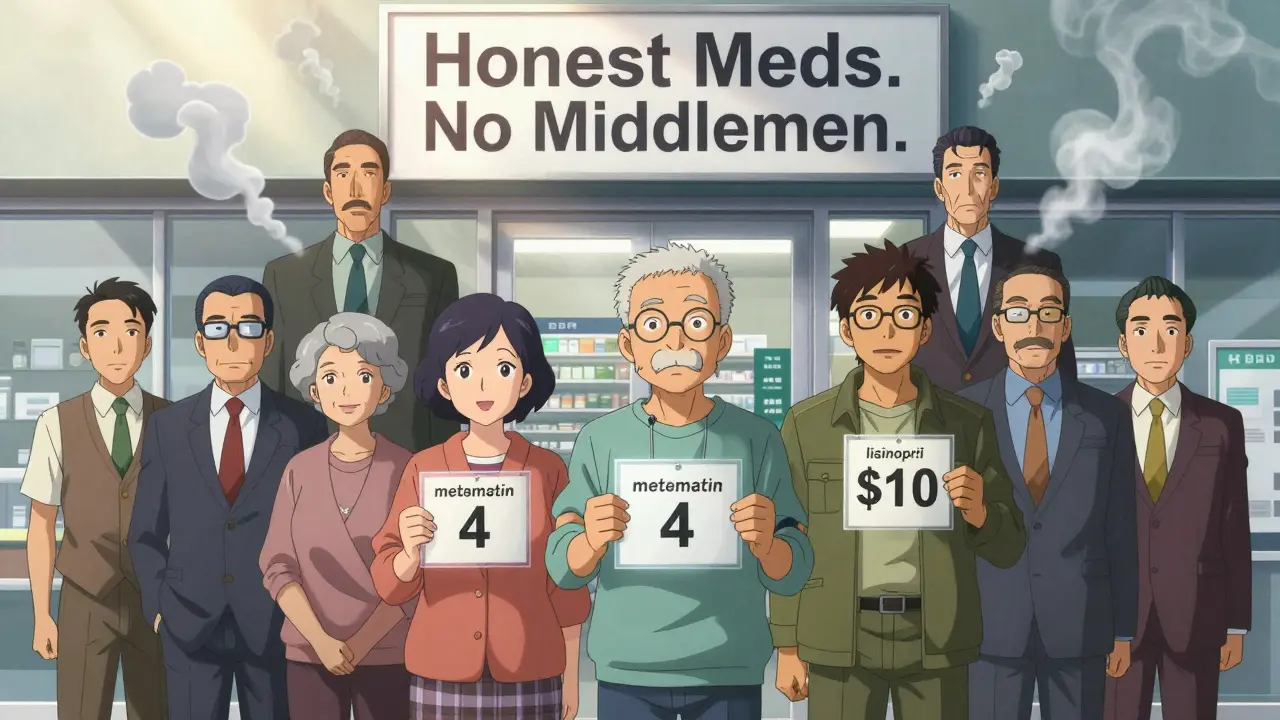

Not all pharmacies are giving up. A growing number are changing their model entirely. Some are ditching PBMs and going direct-to-consumer. Mark Cuban’s Cost Plus Drug Company charges $20 for a generic plus a $3 dispensing fee. No spreads. No clawbacks. Just transparent pricing. As of mid-2024, they’ve filled over a million prescriptions. Others are shifting to medication therapy management (MTM). Instead of just filling scripts, pharmacists now spend 30 minutes with patients reviewing all their meds, checking for interactions, and helping them save money. Medicare pays for this service. It’s not a huge profit-but it’s stable. Pharmacies that added MTM saw net margins jump from 1.5% to 4-6%. A few are even offering cash-pay generics. If you don’t have insurance, you pay $5 for metformin, $10 for lisinopril. No PBM. No middleman. Just the cost of the pill and a small fee to cover labor. It’s not for everyone-but it’s working in communities where people are priced out of traditional insurance.

What’s Next? Regulatory Pressure and New Models

The government is starting to pay attention. The FTC held a workshop in 2023 focused on pharmacy reimbursement practices. Several states-California, Texas, Illinois-have passed laws requiring PBMs to disclose how much they’re reimbursing pharmacies. The Inflation Reduction Act’s drug price negotiation rules (starting in 2026) may indirectly help by lowering overall drug costs. But the real change will come from consumers. More people are asking: “Why does this $1 generic cost me $15?” When patients start demanding transparency, the system will have to respond. Amazon Pharmacy now shows exact drug costs before checkout. Walmart’s $4 generic list is public. Even CVS now offers a “price transparency” tool on its app. The future belongs to pharmacies that stop competing on price alone and start competing on trust. That means clear pricing, honest conversations, and services that add real value-not just pills in a bottle.What This Means for Patients

You might be wondering: “Should I avoid generics?” Absolutely not. Generics are safe, effective, and save billions every year. But you should know how the system works. If you’re on a fixed income, ask your pharmacist: “Is there a cash price for this?” Often, it’s cheaper than your copay. If you’re using mail-order, compare the total cost to your local pharmacy. Sometimes, the convenience isn’t worth the markup. And if you’re frustrated by rising prices, talk to your local pharmacy. Ask why your co-pay went up. Ask if they’re being clawed back. Your voice matters more than you think.Why do pharmacies make more profit on generics than brand-name drugs?

Generics cost much less to produce and are sold by multiple manufacturers, creating competition that lowers wholesale prices. Pharmacies buy them cheaply and apply a higher percentage markup because the base cost is low. Brand-name drugs, however, are priced high by manufacturers, and pharmacies get fixed reimbursement rates from PBMs that often don’t cover their cost-leading to near-zero or negative margins.

What is spread pricing, and how does it hurt pharmacies?

Spread pricing is when a pharmacy benefit manager (PBM) charges an insurance plan more for a drug than it pays the pharmacy. The difference-called the “spread”-goes to the PBM as profit. For example, the PBM might charge the insurer $12 for a generic but only reimburse the pharmacy $8. The pharmacy never sees the $4 difference, and if the reimbursement rate drops later, they might be forced to pay it back through a clawback.

Why are independent pharmacies closing faster than chain pharmacies?

Independent pharmacies lack the buying power and negotiating leverage of large chains. They can’t secure better reimbursement rates from PBMs, can’t afford to own their own PBM, and struggle with rising overhead. Chains often buy out independents, integrate them into their network, and benefit from economies of scale. Between 2018 and 2023, over 3,000 independent pharmacies closed-most because they couldn’t survive on shrinking generic margins.

Can I save money by paying cash for generics instead of using insurance?

Yes, often. Many pharmacies offer cash prices for common generics that are lower than your insurance copay. For example, metformin might cost $4 cash but $15 with insurance due to high deductibles or PBM spreads. Always ask your pharmacist for the cash price before using insurance-it could save you 50% or more.

Are generic drugs less effective than brand-name drugs?

No. The FDA requires generics to have the same active ingredient, strength, dosage form, and route of administration as the brand-name version. They must also be bioequivalent-meaning they work the same way in the body. The only differences are in inactive ingredients like fillers or dyes, which don’t affect effectiveness. Generics are just as safe and effective, and they’ve saved U.S. patients over $300 billion since 2009.

Nicholas Miter

January 27, 2026 AT 21:25Man, I never thought about how PBMs are the real villains here. I just assumed pharmacies were raking it in. Turns out they’re barely scraping by on generics while the middlemen get fat. Kinda wild when you think about it.

Suresh Kumar Govindan

January 29, 2026 AT 08:23The systemic erosion of pharmaceutical sovereignty is a direct consequence of neoliberal rent-seeking architectures.

James Nicoll

January 30, 2026 AT 11:30So the pharmacy’s profit is basically ‘pay me $5 for a pill that cost me $3’… and the PBM takes $4 from the insurance company that didn’t know it was paying $12? Sounds like a magic trick where the rabbit is your wallet. 🎩💸

Uche Okoro

January 31, 2026 AT 14:23The structural asymmetry in reimbursement mechanisms reflects a pathological concentration of monopsonistic power within the PBM-industrial complex. The marginal utility of generic dispensing has been systematically devalued through regulatory capture and vertical integration.

Peter Sharplin

February 1, 2026 AT 09:14For anyone on a tight budget: always ask for the cash price. I had a friend paying $18 for metformin with insurance - cash was $4. No joke. Pharmacies know this. They just don’t always volunteer it. It’s not complicated, but it’s not obvious either.

John Wippler

February 2, 2026 AT 09:57This isn’t just about drugs - it’s about trust. The pharmacy down the street isn’t some corporate machine. It’s the guy who remembers your kid’s name, who calls you when your script’s ready, who sees you struggling and quietly slips you a discount. That’s worth more than any algorithm-driven mail-order warehouse. We’re losing something real here - not just profits, but connection. Don’t let the convenience of Amazon Pharmacy make you forget that.

And yeah, MTM? That’s the future. Pharmacists aren’t just pill dispensers. They’re health coaches. Let’s start paying them like it.

Faisal Mohamed

February 3, 2026 AT 23:04PBMs = financial vampires 🧛♂️💸

Generics = the last blood source for local pharmacies.

Mail-order = automated soulless profit engine.

Transparency = the only hope.

Also, Mark Cuban is a hero. 🙌

eric fert

February 4, 2026 AT 03:40Okay, but let’s be real - this whole ‘independent pharmacy’ narrative is just nostalgia dressed up as activism. The truth? Most of these little shops were barely functional anyway. Outdated inventory, no EHR, staff who still use paper logs. They weren’t ‘saving the community’ - they were just surviving on outdated business models. The real tragedy isn’t that they’re closing - it’s that people still think they’re somehow ‘better’ just because they’re small. Meanwhile, mail-order pharmacies are using AI to predict refill patterns and reduce waste. They’re not evil - they’re efficient. And efficiency isn’t a sin, it’s progress. Also, ‘cash pricing’? That’s just a gimmick for people who don’t understand insurance networks. You think you’re saving money? You’re just avoiding the system that subsidizes your care. Wake up.

Curtis Younker

February 6, 2026 AT 00:54Guys. I work at a small pharmacy. We lost 80% of our generic margin in five years. We’re down to 1.5% net. But here’s the thing - we started doing MTM sessions. We sit down with people. We check their meds. We help them find cheaper alternatives. We even call their doctors if something looks off. It’s not glamorous. We don’t make a fortune. But we’ve got patients who come in just to say thanks. We’ve got people who trust us. And honestly? That’s worth more than any PBM spread. If you’re a patient - don’t just go to the cheapest place. Go to the one that knows your name. That’s the real value.

Dan Nichols

February 6, 2026 AT 16:34Generics are fine but the system is rigged. PBMs are the real problem. And yeah, cash prices are better but only if you’re lucky enough to live near a pharmacy that still gives a damn. Most don't. They're owned by private equity now. They care about quarterly returns, not your asthma inhaler. Also, why are we still using paper receipts? This is 2024.

Renia Pyles

February 8, 2026 AT 16:08Everyone’s acting like this is some new crisis. It’s not. It’s been happening for 20 years. The only reason you’re noticing now is because your co-pay went up. Meanwhile, the chains are just buying up independents and rebranding them as ‘community pharmacies’ while the real owners sit in New York collecting dividends. Wake up. This isn’t about transparency - it’s about control.

Nicholas Miter

February 9, 2026 AT 01:58^^^ this. And I’ve seen it firsthand - my uncle’s pharmacy got bought by a private equity firm. They kept the sign, the same staff, even the same coffee pot. But now the profit goes to a hedge fund in Delaware. The pharmacy’s still there… but the soul? Gone.